Hawaii’s Trailblazing Solar Market Continues to Struggle Without Net Metering

Aug 8, 2019 05:28 PM ET

Hawaii’s residential solar market continues to contract, a phenomenon the industry largely attributes to policy changes that went into effect after the state ended net energy metering in 2015.

The number of active solar companies on Oahu, the state’s largest market, dropped from 300 in 2015 to just 98 last year, according to the Hawaii Solar Energy Association (HSEA). And in the first half of 2019, total residential PV permits declined about 5 percent, according to numbers compiled by local contractor ProVision Solar.

A post-net-metering falloff in the residential market isn’t exclusive to Hawaii, with Nevada and South Carolina experiencing similar declines after moving to new tariff structures. Still, the choices Hawaii makes in structuring its market could have wide implications, and will be closely watched by the national solar industry.

Hawaii was the first state to adopt a 100 percent renewables standard, and it has outlined a plan to meet those goals in part by outfitting homes with solar and storage. At the end of 2017, distributed solar accounted for the largest portion of Hawaiian Electric Company's renewable portfolio standard attainment, at nearly 10 percent out of 26.8 percent renewable generation.

These days Hawaii has company in its ambitions: Seven other states have passed 100 percent renewable portfolio standards or clean energy requirements. As more states adopt renewables goals, Hawaii has the potential to outline solar and storage tariffs worthy of emulation.

“Hawaii will probably be the first state to have a pretty comprehensive tariff that looks at consumers offering grid services and being a prosumer of electricity instead of just a consumer,” said Will Giese, HSEA’s executive director.

“I just hope that we have a market that can handle it," Giese added.

A depressed market

Hawaii's solar permits have been decreasing since the phaseout of net energy metering (NEM) in 2015. According to Giese, Oahu permits dropped by between one-third and 50 percent from 2015 to 2018.

Giese attributed the “depressed market” almost entirely to the ending of NEM and the creation of new tariff structures, which established more complicated rewards for installing residential solar. He also pointed to the state’s small market size and the limited quantity of companies operating there as further challenges.

So far, the new tariffs appear less enticing to customers. But through 2016, 2017 and even into 2018, the state’s installers were still finishing the last of their NEM systems.

“Now we’re reaching the end of all that backlog,” said Giese. “We’re starting to see a leveling-out of the market.”

A slowdown in permits, and a future lag in installations, may reflect customer responses to the new tariffs.

According to a Greentech Media review of Oahu building permits, permits issued to national leader Sunrun were down about 40 percent in the first seven months of 2019 compared to last year.

Sunrun, which is a member of HSEA and among the top five installers in the state, told Greentech Media that “the permit numbers are not reflective of our company’s actual market size in Hawaii” because they don’t account for permits granted to the local channel partners the company works with.

Giese said the company’s permit falloff is symptomatic of the challenges facing the entire market, as it works to dramatically increase distributed generation and implement a state policy of 100 percent renewables by 2045.

“There’s a bigger issue at play,” said Giese.

So long to the NEM "slam-dunk"

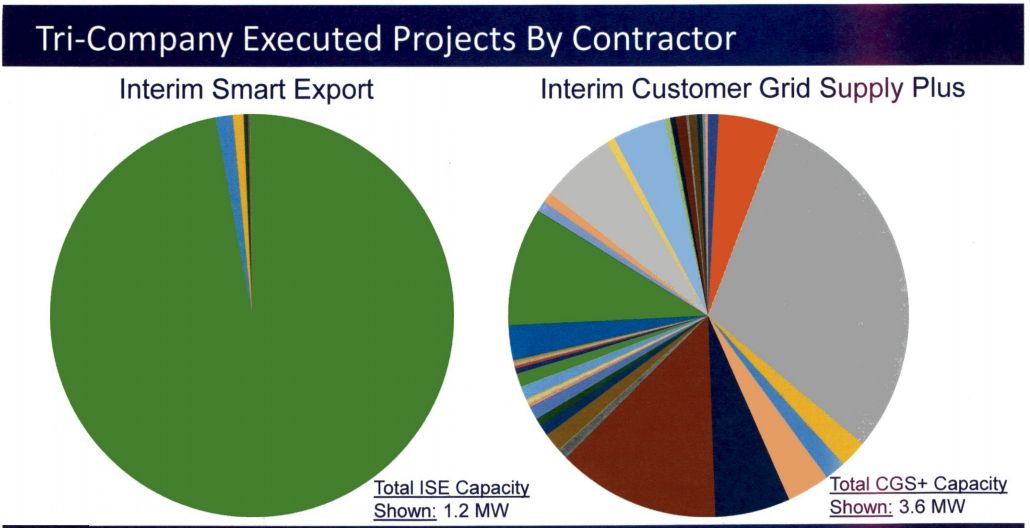

With net metering no longer an option for Hawaii's solar customers, they have two programs to choose from: “Smart Export,” which requires an energy storage system that customers charge during the day and use for power at night, and “Customer Grid Supply Plus,” where they can export power to the grid throughout the day but receive less-enticing compensation.

Rather than the “slam-dunk” sales proposition associated with net metering, ProVision’s president, Marco Mangelsdorf, said the new programs can be confusing to consumers.

“For NEM, it was so damn simple,” said Mangelsdorf. “[For] every kilowatt-hour that you fed into the grid, the homeowner would be compensated.”

By comparison, the new tariff structures established by state regulators can be a hard sell because the economics are more difficult for companies to explain and for consumers to understand.

But Mangelsdorf also said the downturn in permits may signify that Hawaii’s tremendous growth of years past has hit a limit. He said the current pace of permits suggests 2019 will be another low year.

“One can make the case that maybe this is the new normal, for at least the time being, and that the likelihood of going back to the stratospheric numbers between 2011 and 2015…those Pollyanna days are not likely to return,” said Mangelsdorf.

ProVision — a contractor that operates only on the Big Island and competes with Sunrun there — tracks Hawaii permits and tabulated that Sunrun’s losses across Hawaii’s islands are even higher than 40 percent. Mangelsdorf said it's “plausible” that permits from the company’s channel partners could make up its losses. But he argued that’s “unlikely” because the falloff is so steep.

Mangelsdorf suggested Sunrun’s challenges may stem from its dominance in installing Smart Export projects. In a July presentation, Hawaiian Electric Company reported that “currently the program is not working as originally designed.” The presentation also noted that one unidentified contractor was accounting for the vast majority of those projects.

Sunrun declined to comment on its position in the state’s Smart Export market.

Source: Hawaiian Electric Company

While the new structures may have an outsized impact on what Giese calls “the big bear in the room,” he argues it’s not “a Sunrun issue.”

Mangelsdorf said the tariff challenges are impacting many of the residential market’s players as regulators continue to tweak their structure for future iterations.

“The uncertainty and the interim nature of some of these tariffs gives a number of us in the industry cause for grief in terms of what comes next,” said Mangelsdorf. “How can you develop a business model that’s projecting beyond six, 12, 18 months with any confidence when you’re not sure what exactly you’re going to be selling in a year, or two, or three?”

Booms and busts are not uncommon in the solar industry, but Hawaii’s slip in residential solar installation rankings may foreshadow struggles for states pursuing similar policies.

“Ideally we need to make Hawaii the testbed for what is possible for massive amounts of DERs,” said Giese.

“All the companies in the world should be wanting to come to Hawaii to do business here because we are the tip of the spear for DER adoption.”